Debt relief ought to be at the centre of negotiations over a New Deal for Greece. That has been our government’s mantra from 26th of January, our first day on the job. Exactly five months later, on 26th of June, the IMF has conceded the point (as evidenced earlier today by the NYT) – on the very day Prime Minister Alexis Tsipras called for a referendum so that the Greek people could reject an IMF-led proposal that offered no… debt relief.

The IMF’s latest debt sustainability analysis (DSA) is a fascinating read:

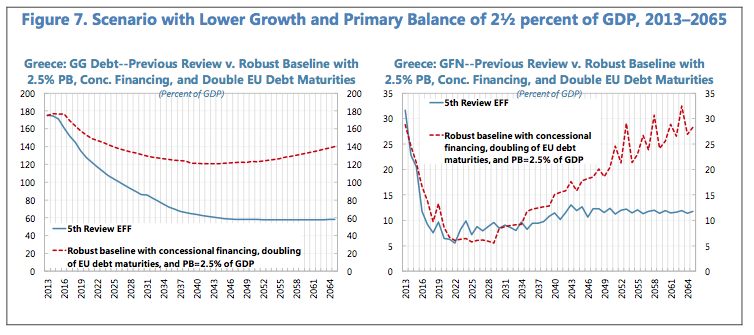

For the first time, the IMF recognised that, in its fifth review assessment, there was a low probability that Greece’s public debt would prove sustainable.

Here is an extract from the IMF’s own report confessing that, to portray Greek public debt as sustainable (without substantial debt relief), its researchers had to make the assumption that “…Greece would go from having the lowest average total factor productivity (TFP) growth in the euro area since it joined the EU in 1981 to having among the highest TFP growth, and that it would go to the highest labor force participation rates and to German employment rates.” Pigs would, of course, sooner fly!

When asked how productivity growth would do the ‘pole vault’ from the euro area’s lowest to the euro area’s highest levels, with employment recovering fully (and in the absence of credit and investment), the IMF’s standard answer is: “To achieve TFP growth that is similar to what has been achieved in other euro area countries, implementation of structural reforms is therefore critical.” But, Chapter 3 of the IMF’s April 2015 World Economic Outlook report tears this assumption to pieces. Indeed, the IMF’s own research shows that labour market reforms have a negative impact on total factor productivity while product market reform has a neutral one.

Returning to Greek public debt sustainability, this latest DSA (debt sustainability analysis) by the IMF could not be blunter. In fact, it is even ‘ruder’ to official Europe, that remains in denial of the need for any debt relief, than we – the SYRIZA government – would imagine being: Without a haircut, the IMF claims, not even fifty years of austerity (i.e. a primary surplus of 2.5%) would suffice to reduce debt to sustainable levels – see graph.

“It is simply not reasonable”, also argues the IMF’s document “to expect the large official sector held debt to migrate back onto the balance sheets of the private sector at rates consistent with debt sustainability”. Of course it is not![1]

EPILOGUE

Puzzlingly, all this fine research by the good people at the IMF suddenly evaporates when IMF functionaries coalesce with their ECB and the European Commission colleagues in order to impose upon our government their chosen policies. On 25th June we were presented with their ultimatum that centred upon zero debt relief, gigantic austerity (3.5% in the medium term), and more of the same labour and product markets’ ‘reforms’.

- Never before has a veritable institution advocated policies that clashed so mercilessly with its own research.

- Never before has the IMF agreed, on economic analysis, with a government it sought to devastate.

[1] One wonders why it migrated to the public sector balance sheet in the first place. Could it be that this was accomplished by the failed IMF-driven programs of 2010 and 2012?